Zero‑Based Budgeting Explained With Examples: The Complete Beginner’s Guide

Financial Guidance Disclaimer

This article provides educational information only and does not constitute financial advice. Financial decisions should be based on your personal circumstances.

Budgets often fail not because people lack willpower, but because the method doesn’t fit their psychology. Traditional budgeting tends to set loose limits and hope for the best. Zero‑based budgeting takes a different approach: it demands that every single dollar you earn has a job before the month begins. That simple shift in mindset can transform a vague sense of financial stress into a clear, actionable plan.

Zero-based budgeting is a budgeting method where every dollar of income is assigned a specific purpose, such as expenses, savings, investments, or debt repayment, until the remaining balance equals zero. A zero balance does not mean spending all your money—it means every dollar has been intentionally allocated.

This guide explains what zero‑based budgeting is, how it works, how to create one, and how to troubleshoot the real‑world curveballs that can derail even the most meticulous plan. Whether you are a student, a freelancer, or a couple juggling family expenses, you’ll find practical examples and strategies you can use today.

What Is Zero‑Based Budgeting?

Zero‑based budgeting is a proactive, rather than reactive, way to manage money. Instead of looking back at what you spent last month and roughly repeating it, you start from zero and decide where every dollar will go in the month ahead. The method gets its name from the bottom line: your income minus your allocations must equal exactly zero.

This concept didn’t start in personal finance. It originated in corporate and government accounting, where managers had to justify every expense from scratch each year rather than simply rolling over the previous year’s budget. Applied to a household, the principle is the same: nothing is automatic. You evaluate every subscription, every grocery bill, every insurance payment, and every savings goal, then assign each dollar accordingly.

The key distinction from a traditional budget is intentionality. A traditional budget might say, “I have $500 left after bills, so I’ll spend less next month.” A zero‑based budget says, “I earned $4,000. Here is exactly where each of those 4,000 dollars is going — including the $300 I’m putting into a car repair fund.”

How Does Zero‑Based Budgeting Work?

At its simplest, zero‑based budgeting follows a repeatable sequence that you can run each month. The framework works regardless of income level.

Calculate your total monthly take‑home pay. Include salary, side‑hustle income, bonuses, government benefits, and any other predictable source of cash. For irregular income, use a conservative estimate based on the lowest recent month.

List every expense category you anticipate. Start with fixed obligations — rent or mortgage, minimum debt payments, insurance premiums — then move to variable costs like groceries, fuel, and entertainment.

Prioritize necessities. Housing, utilities, food, and essential transportation come first. These are non‑negotiable; without them, everything else collapses.

Allocate savings and debt payments beyond the minimums. Treat savings like a bill you owe yourself. This includes emergency funds, retirement contributions, and sinking funds for irregular expenses like car maintenance or holiday gifts.

Assign remaining money to discretionary categories. Streaming services, dining out, hobbies, and other wants get funded only after obligations and savings are covered.

Adjust until the budget reaches exactly zero. If income exceeds expenses, add the surplus to a savings or investment category. If expenses exceed income, reduce discretionary spending until the numbers balance.

The discipline is in the details. You don’t just estimate — you check your actual spending against the plan and adjust in real time.

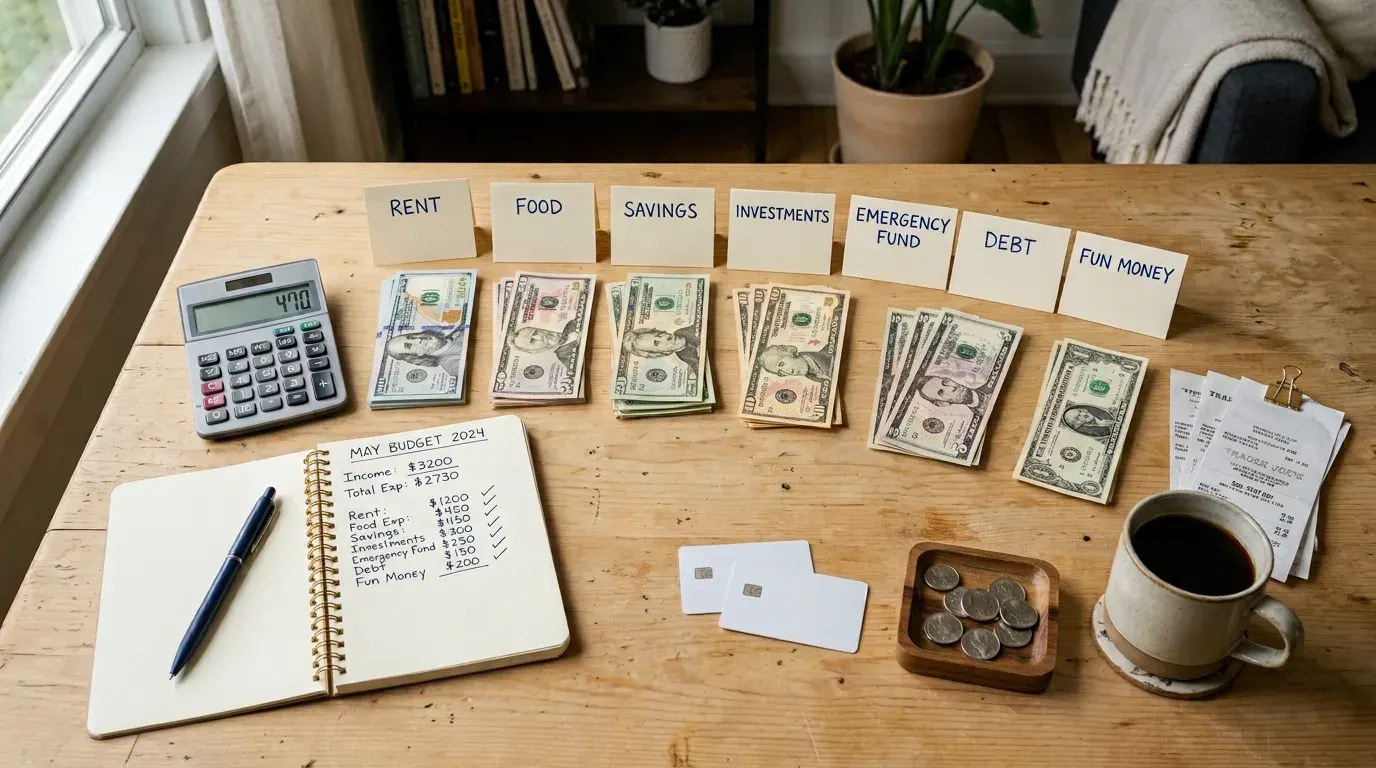

Zero‑Based Budget Example

Below is a worked example for someone earning $4,200 per month after tax, living in a mid‑sized city, with moderate debt and a goal of building an emergency fund.

Category | Amount | Notes |

|---|---|---|

Income | $4,200 | Take‑home pay after taxes |

Essential Expenses | ||

Rent | $1,250 | Fixed |

Utilities (electric, water, internet) | $260 | Variable, averaged |

Groceries | $450 | Household of one |

Transport (gas, insurance, maintenance) | $200 | Car is paid off |

Health insurance | $180 | Through employer |

Minimum debt payments | $300 | Student loan + credit card |

Savings & Investment | ||

Emergency fund | $400 | Building to 3 months of expenses |

$300 | Automated transfer | |

Car maintenance sinking fund | $100 | Irregular expense |

Discretionary | ||

Dining out | $150 | Two meals, one coffee outing per week |

Streaming & subscriptions | $35 | Two services |

Hobbies / entertainment | $100 | Gym, books, weekend activities |

Clothing | $75 | Averaged over year |

Miscellaneous / buffer | $200 | Surprise expenses; if unused, rolls to savings |

Total Allocated | $4,200 | Income minus allocations = $0 |

This individual earns enough to cover essentials and still directs $800 toward savings and debt‑repayment beyond minimums. The miscellaneous buffer provides a cushion; if it goes unspent, it gets redirected to the emergency fund at the end of the month. That’s the zero‑based mindset in action.

Advantages of Zero‑Based Budgeting

Heightened spending awareness. When you account for every dollar, small spending leaks — like a forgotten subscription or an overpriced phone plan — become impossible to ignore. Many people discover they are spending $150 or more each month on things they barely use.

Reduced waste. Because every category is scrutinized each month, you naturally trim expenses that no longer serve you. Unlike a set‑and‑forget budget, zero‑based budgeting forces a monthly audit.

Goal‑oriented saving. Saving becomes deliberate rather than accidental. You decide in advance how much goes toward an emergency fund, a home deposit, or a vacation, and the budget holds you accountable.

Improved cash flow management. Knowing exactly where money is going reduces the risk of overdrafts and missed payments. It also makes it easier to time large expenses around pay periods.

Greater financial discipline. The method instills the habit of planning ahead. After a few months, many people find they make fewer impulse purchases because every dollar already has a purpose.

Accelerated debt repayment. By treating extra debt payments as a mandatory category, zero‑based budgeting can shorten the repayment timeline considerably. Even an extra $100 per month can carve years off a credit card balance.

Disadvantages of Zero‑Based Budgeting

Time commitment. A zero‑based budget requires more upfront effort than a loose spending plan. You’ll need to track expenses, categorize transactions, and adjust throughout the month.

Requires regular updates. Life rarely sticks to a spreadsheet. Car repairs, medical co‑pays, and birthday dinners can throw off even the best plan. Successful zero‑based budgeters review and tweak their budget weekly, not just on the first of the month.

Less flexible for irregular income. Freelancers, commissioned salespeople, and gig workers can find it difficult to plan a month when they don’t know exactly what they’ll earn. A modified approach — budgeting from a conservative baseline and creating a priority list for any surplus — is often necessary.

Can feel restrictive. At first, the level of detail can feel stifling. Some people rebel against it and abandon the method entirely. Building in a reasonable discretionary allowance and a small buffer can ease this feeling.

Learning curve. Getting the categories right, especially in the first few months, involves trial and error. It’s common to underestimate variable expenses and overestimate self‑control in the early stages.

Who Should Use Zero‑Based Budgeting?

The method works well for anyone who wants a granular understanding of their money, but it’s particularly suited to certain situations.

Employees with a stable salary can predict income easily, which simplifies the planning process.

Families juggling multiple expenses benefit from the clarity of seeing exactly how much goes to childcare, groceries, and extracurricular activities.

Students living on a fixed income from loans, part‑time work, or parental support can stretch limited funds further.

People aggressively paying off debt often find zero‑based budgeting the most effective tool because it maximizes every dollar toward principal.

High‑income earners who feel like they should be saving more can uncover unconscious spending that adds up to thousands.

Retirees managing withdrawals from savings can use the method to ensure their nest egg lasts.

Freelancers and those with highly variable income can still use zero‑based budgeting, but they need to base the month on a conservative income estimate and create a priority list — essentials first, then savings, then wants — so that any extra income is deployed intentionally.

Fixed vs Variable Expenses

Understanding which costs are stable and which fluctuate is fundamental to building an accurate zero‑based budget.

Fixed expenses remain the same each month: rent, mortgage, car payments, insurance premiums, and subscription fees. They are predictable and form the backbone of your budget.

Variable expenses change from month to month: groceries, electricity, fuel, dining out, and entertainment. These require estimation based on historical spending, but they are also where most people find room to cut.

Essential vs discretionary is another useful cut. Food is essential; restaurant meals are discretionary. Electricity is essential; a premium streaming package is not. A zero‑based budget forces you to make these distinctions explicit.

Expense Type | Examples | Budgeting Strategy |

|---|---|---|

Fixed essential | Rent, insurance, minimum debt payments | Pre‑assign exact amounts |

Variable essential | Groceries, fuel, utilities | Estimate based on past 3 months; adjust during review |

Fixed discretionary | Subscriptions, gym membership | Question if they’re still needed |

Variable discretionary | Dining out, entertainment, hobbies | Set a hard cap; track weekly |

Savings and Financial Goals in a Zero‑Based Budget

A frequent misunderstanding is that zero‑based budgeting only covers bills. In truth, it’s one of the most effective ways to prioritize saving because you treat savings as a line item rather than hoping something is left over.

Emergency fund. Financial educators often recommend building a starter fund of $500 to $1,000, then expanding it to three to six months of essential expenses. Your zero‑based budget can include a monthly contribution until you hit the target.

Retirement savings. If your employer offers a retirement plan with a match, contributing enough to capture the full match should be a high‑priority line item. Additional contributions can go to an IRA or similar vehicle.

Sinking funds. These are savings buckets for predictable but irregular expenses: car repairs, annual insurance premiums, holiday gifts, medical deductibles. Instead of being caught off‑guard, you set aside a small amount each month. If your car insurance is $600 every six months, a $100 monthly sinking fund ensures the bill is covered when it arrives.

Goal‑specific savings. Whether it’s a vacation, a wedding, or a home down payment, assigning a category in your zero‑based budget makes the goal tangible and the progress measurable.

Zero‑Based Budgeting vs Other Budgeting Methods

Different budgeting methods suit different personalities. The table below compares zero‑based budgeting with four common alternatives.

Method | Core Principle | Best For | Drawbacks |

|---|---|---|---|

Zero‑Based | Assign every dollar a job; income minus allocations equals zero | Detail‑oriented planners, debt payoff | Time‑intensive |

50/30/20 | 50% needs, 30% wants, 20% savings/debt | Beginners who want simplicity | Can oversimplify; doesn’t account for high‑cost areas |

Envelope System | Use cash envelopes for each category; stop spending when empty | People who struggle with overspending on cards | Impractical for online payments; less granular |

Pay‑Yourself‑First | Automate savings first; spend the rest freely | Savers who want a low‑effort approach | May not curb overspending in non‑savings categories |

Values‑Based | Align spending with personal values rather than strict categories | People with non‑traditional financial goals | Can be subjective and hard to track |

Zero‑based budgeting is often the most powerful for people who want a high degree of control and are willing to invest the time. However, hybrids work well too — you might use a zero‑based budget for essentials and savings, then apply a 50/30/20 lens to the remainder.

Common Zero‑Based Budgeting Mistakes

Even enthusiastic budgeters make errors that can derail the whole process.

Forgetting irregular expenses. Annual subscriptions, car registration renewals, and holiday spending don’t appear every month, but they will appear eventually. Sinking funds prevent these from becoming budget emergencies.

Setting unrealistic spending limits. If you currently spend $600 on groceries and slash the category to $350 overnight, you are setting yourself up for failure. Gradual adjustments based on real data are more sustainable.

Ignoring emergency savings. Some people get so focused on eliminating debt that they neglect the emergency fund. Without one, a single unexpected expense can push them back onto credit cards.

Not reviewing the budget during the month. A zero‑based budget isn’t a set‑and‑forget document. Regular check‑ins — even five minutes a week — catch overspending early and allow you to reallocate unused money before the month ends.

Overspending categories without adjusting others. If you blow past your dining‑out budget, you must subtract the overage from another category, not just let the budget slide. Failing to do this breaks the zero‑based structure.

Giving up after one bad month. Perfection isn’t the goal. A month where you overspend is data, not a verdict. Many successful budgeters say it took three to four months to dial in the numbers.

How to Create a Zero‑Based Budget

This step‑by‑step framework works whether you use a spreadsheet, a notebook, or a budgeting app.

Calculate monthly income. Use your after‑tax, take‑home pay. If you have irregular income, use a conservative average of the last six months.

Track current spending for at least one month. Go through bank and credit card statements to see where your money actually goes. Don’t guess.

Categorize expenses. Group them into fixed essential, variable essential, fixed discretionary, variable discretionary, savings, and debt.

Prioritize essentials. Housing, utilities, food, basic transport, and minimum debt payments get funded first.

Allocate savings. Decide how much goes to emergency fund, retirement, sinking funds, and goal‑specific savings. Treat these as fixed expenses.

Assign remaining dollars to discretionary categories. Be specific: “dining out $120” instead of “fun money $300.”

Balance to zero. If expenses exceed income, cut from discretionary categories. If income exceeds expenses, pour the surplus into your highest‑priority savings or debt goal.

Review weekly. Compare actual spending to your plan and reallocate as needed. Use any leftover money in a category at month‑end to accelerate savings or debt payoff.

Real‑World Examples

1. College Student Managing a Tight Budget

Jamie is a full‑time student with a part‑time job bringing in $1,200 a month. Her zero‑based budget covers rent ($500, shared apartment), groceries ($200), utilities ($60), phone ($40), and transport ($50). She allocates $100 to a tuition book sinking fund, $50 to an emergency fund, and leaves $200 for discretionary spending, which includes a streaming service, a couple of meals out, and thrift‑store clothing. Every dollar has a home, and she avoids the credit card debt that traps many of her peers.

2. Family Reducing Monthly Expenses

The Patel family brings in $6,500 per month. Their mortgage is $1,800, childcare $1,200, and groceries were running $1,100. After tracking expenses for a month, they realized they were spending $300 on impulse food delivery. They cut that to $100, redirected $100 to a vacation sinking fund, and added the remaining $100 to their emergency fund. Their zero‑based budget now shows every dollar’s destination, and they’ve saved $2,400 in the first year from that one adjustment.

3. Freelancer with Irregular Income

Aisha is a freelance graphic designer whose monthly income ranges from $2,500 to $5,000. She builds her zero‑based budget around her lowest recent month ($2,500). That covers rent, utilities, groceries, transport, insurance, and minimum debt payments. She then creates a priority list for any surplus: first, a larger payment toward her credit card; second, a contribution to her emergency fund; third, a small personal allowance. In months where she earns $4,000, the extra $1,500 gets allocated according to the list — no impulse spending.

4. Couple Saving for a Home Deposit

Lucia and Ben earn a combined $8,400 a month. They use a zero‑based budget that funds their rent ($2,100), living expenses, and debt payments, then allocates $2,000 to a high‑yield savings account for a down payment. They treat this transfer like a bill. After two years, they have saved $48,000 — enough for a 10% down payment on their target home — without having to cut out every small enjoyment because the budget gave them permission to spend within set limits.

Best Tools for Zero‑Based Budgeting

You don’t need specialized software, but the right tool makes the process smoother.

Spreadsheet templates (Google Sheets, Excel) give complete flexibility. You can build your own or start from a free template and adapt it as your categories evolve. The manual entry keeps you intimately connected with your spending.

Budgeting apps often have zero‑based features built in, connecting to your bank accounts to automatically import transactions and track category balances. The CFPB notes that digital tools can help people stay engaged with their finances, as long as the tool supports the budgeting method rather than dictating it.

Pen and paper. A simple notebook with income at the top and expenses listed below works for those who prefer a tangible, screen‑free approach. The act of writing can reinforce commitment.

Whichever tool you choose, the method — not the app — is what drives results. A free spreadsheet maintained with consistency will outperform a premium app used sporadically.

Frequently Asked Questions

What is zero‑based budgeting?

Zero‑based budgeting is a method where you assign every dollar of income to a specific expense, savings, or debt category until there is zero left unallocated. It forces intentional spending and saving, unlike traditional budgeting that often leaves leftover money unaccounted for.

Why is it called zero‑based?

The name comes from the bottom‑line result: income minus all allocations equals exactly zero. It does not mean your bank account drops to zero; it means no money is left without a designated purpose, whether that purpose is spending, saving, or investing.

Is zero‑based budgeting good?

For many people, yes. It provides a granular level of financial control that can accelerate savings and debt reduction. The trade‑off is that it requires regular time and attention. Its effectiveness depends on whether you are willing to track and adjust your budget weekly.

Who should use zero‑based budgeting?

It works well for salaried employees, families, students, and anyone with stable income who wants detailed financial oversight. Freelancers and those with variable income can also use it successfully with modifications, such as budgeting from a conservative baseline.

Does zero‑based budgeting mean spending all my money?

No. It means assigning every dollar a role, which often includes significant allocations to savings, investments, emergency funds, and sinking funds. Spending all your money on consumption would leave nothing for the future, which is not the goal of the method.

How do I budget irregular income with zero‑based budgeting?

Use your lowest recent monthly income as the baseline for essential expenses and savings. When you earn more, allocate the surplus according to a pre‑written priority list — for example, extra debt payments first, then savings, then discretionary spending. This prevents lifestyle inflation.

Can I save money with this method?

Absolutely. By treating savings as a mandatory budget line item rather than an afterthought, zero‑based budgeting often increases savings rates. Many people discover they are able to save more than they thought possible simply by cutting small, unnoticed expenses.

What if my expenses change during the month?

You adjust the budget. Zero‑based budgeting requires regular check‑ins. If you overspend in one category, you reduce another to compensate. Surprise expenses can be covered by a miscellaneous buffer or by temporarily pulling from a sinking fund.

Is zero‑based budgeting better than the 50/30/20 rule?

Neither is universally better. The 50/30/20 rule is simple and low‑effort but less precise. Zero‑based budgeting offers more control and works better for people with specific financial goals. Some people blend the two, using zero‑based for necessities and savings and 50/30/20 for discretionary.

How often should I update my zero‑based budget?

At minimum, you should update it once a month before the month begins. However, a weekly 10‑minute review to compare actual spending with planned amounts helps catch problems early and keeps you on track.

What are sinking funds?

Sinking funds are savings buckets for predictable but irregular expenses, such as car repairs, annual insurance premiums, or holiday gifts. Instead of scrambling when the bill arrives, you set aside a small amount each month, smoothing out your budget and avoiding debt.

Can couples use zero‑based budgeting?

Yes. It can be especially helpful for couples because it requires open communication about financial priorities. Many couples hold a monthly budget meeting to review the previous month and plan the next one, ensuring both partners agree on where the money goes.

What happens if I overspend a category?

You must immediately reduce another category to cover the overage. If you don’t, the zero‑based balance breaks, and the unplanned spending essentially becomes debt. A small miscellaneous buffer can absorb minor oversights, but larger overages require real‑time adjustments.

Can businesses use zero‑based budgeting?

Yes, the concept originated in business and government. Companies use it to justify each department’s expenses from scratch each year. In personal finance, the same principle is applied to household spending, ensuring every dollar is scrutinized.

Is zero‑based budgeting difficult to start?

The first month can be challenging because you are building new habits and guessing at variable expenses. However, after two or three months of collecting data, the process becomes routine. Most people find the hardest part is simply starting.

What budgeting tools work best?

Spreadsheets, mobile budgeting apps, and even pen‑and‑paper notebooks can all work. The best tool is the one you will consistently use. Many people start with a simple spreadsheet and later move to an app for automatic transaction tracking.

Should I include investments in my zero‑based budget?

Yes. Retirement contributions, brokerage deposits, and other investments should be line items in your budget, treated as non‑negotiable expenses. This ensures you are building long‑term wealth rather than only managing day‑to‑day spending.

How do I budget bonuses or windfalls?

Decide in advance what percentage goes to each priority. For example, 50% to debt repayment, 30% to savings or investment, and 20% for discretionary enjoyment. This prevents a lump sum from evaporating without a trace, which is a common financial pitfall.

Can retirees use zero‑based budgeting?

Yes, it can help retirees manage withdrawals from retirement accounts and ensure their savings last. By assigning every dollar of monthly income — from pensions, Social Security, and portfolio withdrawals — retirees can track spending closely and adjust as needed.

What is the biggest mistake beginners make?

The biggest mistake is giving up after an imperfect month. Zero‑based budgeting is a skill that improves with practice. A month where you overspend in a few categories is not a failure; it’s an opportunity to refine your estimates and build a more realistic plan next time.

Table 1 — Zero‑Based Budget Overview

Feature | Description | Benefit |

|---|---|---|

Every dollar assigned | Income minus allocations equals zero | Eliminates unplanned spending |

Proactive planning | Budget is created before the month begins | Reduces financial surprises |

Integrated savings | Savings and investments are line items | Ensures long‑term goals are funded |

Flexible categories | Adjust during the month as needed | Adapts to real‑life changes |

Expense scrutiny | All spending is justified each month | Cuts waste and subscription creep |

Table 2 — Monthly Zero‑Based Budget Example

Category | Amount | Notes |

|---|---|---|

Income | $4,200 | After‑tax take‑home pay |

Rent | $1,250 | Fixed |

Utilities | $260 | Averaged |

Groceries | $450 | Tracked weekly |

Transport | $200 | Gas, insurance, maintenance |

Health insurance | $180 | Employer plan |

Minimum debt payments | $300 | Loan + card |

Emergency fund | $400 | Building to 3‑month target |

$300 | Automated transfer | |

Car maintenance sinking fund | $100 | Irregular expense |

Dining out | $150 | Weekly budget |

Subscriptions | $35 | Two services |

Hobbies / gym | $100 | Monthly |

Clothing | $75 | Averaged |

Miscellaneous buffer | $200 | Cushion; unspent rolls to savings |

Total | $4,200 | Income – allocations = $0 |

Table 3 — Fixed vs Variable Expenses

Expense Type | Examples | How to Budget |

|---|---|---|

Fixed essential | Rent, insurance, minimum debt | Assign exact amount |

Variable essential | Groceries, fuel, electricity | Average 3 months; review monthly |

Fixed discretionary | Subscriptions, gym | Re‑evaluate quarterly |

Variable discretionary | Dining out, hobbies, travel | Set a hard cap; track weekly |

Table 4 — Zero‑Based Budgeting vs Other Methods

Method | Core Principle | Best For | Drawbacks |

|---|---|---|---|

Zero‑Based | Assign every dollar; bottom line is zero | Detail‑oriented planners | Time‑consuming |

50/30/20 | 50% needs, 30% wants, 20% savings | Beginners, simplicity | Can oversimplify |

Envelope System | Cash in envelopes, stop when empty | Overspenders | Impractical online |

Pay‑Yourself‑First | Automate savings, spend rest freely | Low‑effort savers | May not control spending |

Values‑Based | Align spending with values | Non‑traditional goals | Subjective tracking |

Table 5 — Advantages and Disadvantages of Zero‑Based Budgeting

Advantages | Disadvantages |

|---|---|

Heightened spending awareness | Time commitment |

Reduced waste | Requires regular updates |

Goal‑oriented saving | Less flexible for irregular income |

Improved cash flow | Can feel restrictive |

Accelerated debt repayment | Learning curve |

Table 6 — Common Budgeting Mistakes

Mistake | How to Avoid |

|---|---|

Forgetting irregular expenses | Use sinking funds |

Unrealistic spending limits | Base limits on past data |

Ignoring emergency savings | Make it a fixed line item |

Not reviewing mid‑month | Schedule a weekly 10‑minute check |

Overspending without adjusting | Reallocate immediately |

Quitting after one bad month | Treat as feedback, not failure |

Table 7 — Budget Categories Checklist

Category Type | Examples |

|---|---|

Housing | Rent/mortgage, property tax, maintenance |

Utilities | Electricity, water, gas, internet, phone |

Food | Groceries, dining out, work lunches |

Transportation | Car payment, fuel, insurance, public transit |

Health | Insurance premiums, prescriptions, dental |

Debt | Minimum payments, extra principal |

Savings | Emergency fund, retirement, sinking funds |

Personal | Clothing, grooming, hobbies |

Entertainment | Streaming, movies, travel |

Miscellaneous | Buffer for unplanned expenses |

Table 8 — Monthly Budget Review Checklist

Task | Why It Matters | Frequency |

|---|---|---|

Compare actual vs planned spending | Identifies overspending early | Weekly |

Reallocate unused funds | Prevents wasted surplus | Weekly |

Review sinking fund balances | Ensures irregular bills are covered | Monthly |

Adjust categories for next month | Keeps budget realistic | Monthly |

Discuss with partner (if applicable) | Maintains alignment on goals | Monthly |

Check progress toward savings goals | Keeps motivation high | Monthly |

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, tax, or investment advice. Budgeting strategies should be adapted to individual circumstances, financial goals, income, and obligations. Consider consulting a qualified financial professional if you need advice tailored to your situation.

Recommended Articles

The Complete Guide to Budgeting for Beginners

Budgeting isn’t about restriction—it’s about clarity. A realistic, no-shame guide for beginners to understand where your money goes, build a system that sticks, and finally end the guilt cycle.

50/30/20 Budget Rule Explained (With Real-Life Examples)

Struggled with budgets that never stick? Learn the 50/30/20 rule with real-life examples, honest limitations, and practical steps to finally take control of your money.