Envelope Budgeting Method: How It Works (Complete Beginner's Guide)

Financial Guidance Disclaimer

This article provides educational information only and does not constitute financial advice. Financial decisions should be based on your personal circumstances.

Budgeting often fails not because people lack intention, but because money feels abstract. When you swipe a card, the cost registers as a number on a screen, not as cash leaving your hand. The Envelope Budgeting Method solves that problem by making spending tangible. It’s one of the oldest personal finance strategies, and for many people, it’s still one of the most effective.

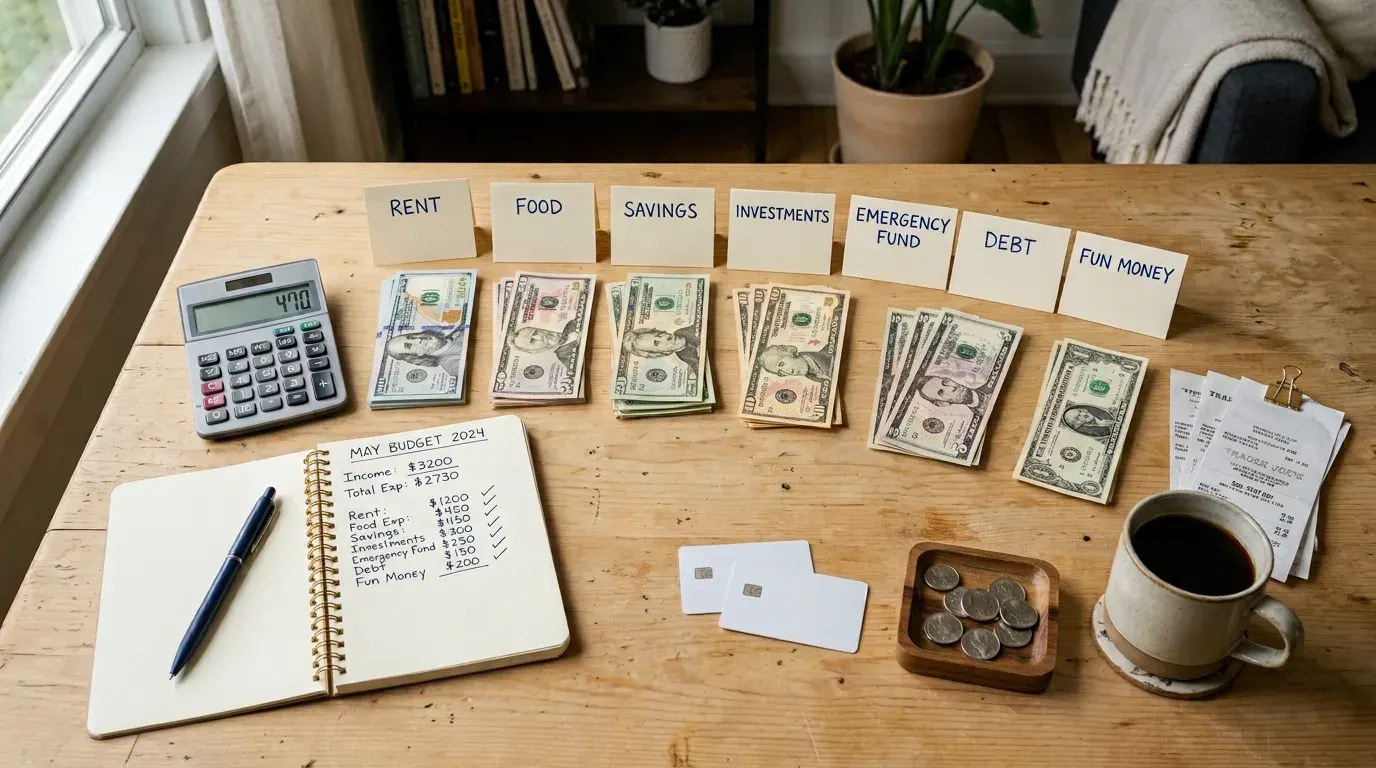

The Envelope Budgeting Method is a budgeting system that divides income into spending categories using physical or digital envelopes. Each envelope holds a set amount of money for a specific expense, helping people avoid overspending and manage their finances more effectively. It works on a simple principle: when the envelope is empty, spending in that category stops. This guide explains exactly how the method works, who it suits, its advantages and drawbacks, and how to get started today—whether you prefer cash or a digital approach.

What Is the Envelope Budgeting Method?

The Envelope Budgeting Method is a cash‑based spending plan where you allocate your take‑home pay into clearly labeled envelopes, each representing a budget category. Once the cash in an envelope is gone, you cannot spend any more in that category until the next budgeting period—typically the following month. You do not borrow from other envelopes, and you do not use credit cards to fill the gap.

The method dates back to a time when most people were paid in cash and bills were settled at the kitchen table. It gained modern popularity through financial educators who recognized that physically handling money creates a psychological barrier to overspending. Unlike a spreadsheet that shows a balance, an empty envelope is an immediate, tangible signal that you’ve reached your limit.

The key difference from a traditional budget is enforcement. A line‑item budget tells you that you’ve allocated $400 for groceries. An envelope shows you exactly how much is left—and when it’s gone, it’s gone.

How the Envelope Budgeting Method Works

Implementing the envelope system follows a repeatable sequence. Here is the step‑by‑step process:

Calculate your monthly take‑home pay. Use the amount that actually lands in your bank account after taxes and deductions. If you have irregular income, estimate a conservative baseline based on the lowest recent month.

List every expense category for the month. Start with fixed obligations like rent or mortgage, utilities, insurance, and minimum debt payments. Then add variable expenses: groceries, transport, dining out, entertainment, personal care, and any other regular spending.

Create spending categories and set amounts. Assign a dollar figure to each category. Fixed expenses often stay the same each month. Variable expenses require a realistic estimate—look at past bank statements if you’re unsure.

Fill the envelopes. If you’re using cash, withdraw the total budgeted amount and physically place the assigned bills into each labeled envelope. If you’re using a digital system, move the designated sums into separate sub‑accounts or track them in a spreadsheet that mimics the envelope structure.

Spend only from each envelope. Throughout the month, pay for items using the money from the corresponding envelope. If you buy groceries, take cash from the “Groceries” envelope. If you dine out, use the “Dining Out” envelope.

Stop spending when an envelope is empty. This is the core rule. There is no borrowing from another category unless you make a conscious decision to adjust the budget—ideally before the spending happens, not after.

Review and adjust monthly. At the end of the month, examine what worked and what didn’t. If you consistently run out of grocery money, either increase that envelope (by reducing another) or find ways to cut costs. Reset the envelopes for the new month with fresh allocations.

This workflow forces active decision‑making. Every purchase gets weighed against the remaining balance in the envelope, which naturally curbs impulse spending.

Physical vs Digital Envelope Budgeting

The envelope method started with paper and cash, but it has evolved. Today, you can use cash, digital apps, bank account sub‑categories, or a spreadsheet. The right version is the one you’ll stick with.

Feature | Physical Cash Envelopes | Digital Envelope Apps | Bank Sub‑Accounts | Spreadsheet Tracking |

|---|---|---|---|---|

Ease of use | Simple, tactile | Requires app setup and linking | Requires bank that offers sub‑accounts | Manual entry; customizable |

Security | Cash can be lost or stolen | App‑protected, but digital risk | Bank‑level security | Depends on device security |

Convenience | Inconvenient for online purchases | Convenient for card‑based and online spending | Works with existing bank cards | Manual; best for planning, not daily spending |

Spending awareness | Very high; physical money feels real | Moderate; notifications can remind you | Low unless actively monitored | High if updated consistently |

Best for | People who overspend with cards; visual learners | Tech‑savvy users; people who rarely use cash | Those who want automatic tracking | Budgeters who enjoy the process of updating |

Drawbacks | Can’t be used for automatic bill payments | Monthly subscription fees on some apps | Not all banks offer envelope features | Time‑consuming to maintain |

Many people blend approaches. For example, they might use cash envelopes for variable daily spending (groceries, dining out, personal care) while keeping fixed expenses like rent and utilities in a bank account with automatic payments. The envelope method doesn’t demand purity—it demands intentionality.

Common Envelope Categories

There is no universal set of envelopes. Your categories should reflect how you actually spend money. That said, most people find the following buckets useful as a starting point.

Category | Description | Example Monthly Allocation |

|---|---|---|

Groceries | Food and household consumables | $500 |

Rent/Mortgage | Housing payment | $1,200 |

Utilities | Electricity, water, gas, internet, phone | $300 |

Transportation | Fuel, public transit, parking, basic maintenance | $200 |

Dining Out | Restaurants, takeout, coffee shops | $150 |

Entertainment | Movies, streaming, concerts, hobbies | $100 |

Shopping | Clothing, electronics, home goods | $100 |

Healthcare | Prescriptions, co‑pays, dental | $100 |

Personal Care | Haircuts, grooming, toiletries | $75 |

Savings | Emergency fund, short‑term goals | $400 |

Insurance | Health, auto, life premiums | $250 |

Debt Payments | Credit cards, loans above minimums | $300 |

Children’s Expenses | School supplies, activities, child care | $250 |

Miscellaneous | Small irregular expenses, buffer | $100 |

This example shows a total allocation of $4,025 for a hypothetical household. The amounts are illustrative; your numbers will differ based on your income, cost of living, and family size. The crucial step is that every dollar of take‑home pay is assigned to an envelope. If income exceeds the allocations, the surplus goes into a “buffer” or extra savings envelope. If expenses exceed income, you must cut back somewhere.

Benefits of Envelope Budgeting

The method’s staying power comes from how it changes spending behavior, not just the math.

Heightened spending awareness. Physically taking cash from an envelope makes the cost of a purchase concrete. Research in behavioral economics consistently shows that people spend less when using cash compared to cards because the pain of paying is more immediate.

Improved discipline. The rule is simple: when the envelope is empty, you stop. There’s no grey area, which reduces the mental negotiation that often leads to overspending.

Reduced impulse purchases. If you see only $35 left in your dining‑out envelope on the 20th of the month, you’re far less likely to grab an unplanned takeaway.

Easier expense tracking. You don’t need to log every transaction into an app. The cash left in the envelope tells you how much you’ve spent and how much remains.

Debt reduction support. By capping spending categories, envelope budgeting frees up money for debt repayment. It also prevents the new debt that comes from using credit cards to cover gaps.

Better savings habits. Savings gets its own envelope—or several. Treating savings as a non‑negotiable expense helps build an emergency fund and reach goals faster.

Less financial stress. When you know exactly how much you can spend in each category, the anxiety of “Can I afford this?” diminishes. The decisions are already made.

Drawbacks of Envelope Budgeting

No budgeting method works perfectly for everyone. Envelope budgeting has genuine limitations.

Cash handling inconvenience. Carrying significant amounts of cash can be impractical and feels unsafe to some. Paying for online purchases with physical cash also requires extra steps—like depositing the money first.

Not ideal for shared households. If two people are spending from the same envelope, tracking who took what can become messy. Clear communication or separate envelopes for each partner can help, but it adds complexity.

Variable expenses are tricky to predict. Some categories, like utilities or medical costs, fluctuate month to month. Envelopes work best when you can estimate reasonably accurately or when you build in a buffer.

Risk of lost or stolen cash. Unlike a bank account, cash in an envelope isn’t insured. While the risk is often low for small amounts kept at home, it’s a consideration that shouldn’t be ignored.

Time commitment. Setting up the envelopes, withdrawing cash, and reconciling at the end of the month takes more hands‑on time than a fully automated budgeting system.

Can feel overly restrictive. For some people, the rigidity of the system is motivating. For others, it feels punitive, leading them to abandon budgeting altogether.

Acknowledging these drawbacks doesn’t invalidate the method; it just means you should adapt the system to your comfort level and life circumstances.

Who Should Use Envelope Budgeting?

The envelope method shines in specific situations and for particular personality types.

It works well for:

Overspenders who lose track of where their money goes. The physical limit of an empty envelope is a powerful brake.

Beginners who have never budgeted before. It’s intuitive and doesn’t require complex calculations.

Families managing multiple spending categories. Envelopes make the family budget visible and shareable.

Students with limited income and a need for strict spending control.

People repaying debt who need to squeeze every dollar toward principal.

Those on low to moderate incomes where every purchase matters.

Cash spenders who find that cash helps them stay on track better than cards.

It may not suit:

People who value convenience above all else, as cash handling takes time.

Those who do most of their spending online, where cash is impractical.

High‑income earners with very stable finances who prefer a lighter‑touch approach.

People who are uncomfortable keeping cash at home.

The method isn’t a moral test. If it helps you spend less and save more, use it. If it creates stress, explore alternatives.

Envelope Budgeting vs Other Budgeting Methods

Different budgeting approaches work for different mindsets. Here’s how envelope budgeting stacks up.

Feature | Envelope Budgeting | Zero‑Based Budgeting | 50/30/20 Budget | Pay‑Yourself‑First | Traditional Budget |

|---|---|---|---|---|---|

Difficulty | Low to medium | Medium to high | Low | Low | Low |

Flexibility | Low (rigid categories) | Medium (adjusts monthly) | High | High | Medium |

Best for | Overspenders, hands‑on budgeters | Detail‑oriented planners | Beginners, simplicity | Savers, busy professionals | People who want a light framework |

Cash usage | High (physical) or digital | Any | Any | Any | Any |

Spending control | Very high | High | Moderate | Low to moderate | Low |

Automation | Low | Can be automated | Can be automated | High (saving is automated) | Low to medium |

Ideal users | Visual, tangible learners | Those who want complete control | Those new to budgeting | Those who want minimal effort | Those who want loose guidance |

Envelope budgeting is essentially a variation of zero‑based budgeting—every dollar has a job—but with the added enforcement mechanism of cash or digital envelopes. The 50/30/20 rule provides a broad framework but little spending control. Pay‑yourself‑first prioritizes savings but doesn’t cap discretionary spending. The envelope method is unique in its focus on limiting spending rather than just tracking it.

Step‑by‑Step Example

Examples make the method concrete. Here are four realistic scenarios, each showing how a different person or household might implement the envelope system. All figures are in U.S. dollars for illustration.

Example 1: College Student

Jaden, a full‑time student with a part‑time job, takes home $1,200 a month. His expenses are modest, but he’s prone to blowing money on food delivery and video games. He decides to use cash envelopes for variable spending while keeping rent and bills on autopay.

Envelope | Monthly Amount |

|---|---|

Rent (autopay) | $500 |

Utilities/Phone (autopay) | $100 |

Groceries (cash) | $250 |

Gas (cash) | $60 |

Dining Out (cash) | $80 |

Entertainment (cash) | $60 |

Books/Supplies (cash) | $50 |

Emergency Savings (automatic transfer) | $100 |

Total | $1,200 |

Jaden withdraws the cash amounts at the start of the month. He’s found that when he orders food delivery through an app, it’s too easy to overspend; with cash, he has to physically hand over the money, which makes him think twice.

Example 2: Single Professional

Mia earns $4,000 after tax as a graphic designer. She’s debt‑free and wants to save for a down payment on a house. She uses a digital envelope app because she rarely carries cash.

Envelope | Monthly Amount |

|---|---|

Rent | $1,400 |

Utilities | $200 |

Groceries | $450 |

Transport (public) | $120 |

Dining Out | $200 |

Entertainment | $150 |

Shopping/Clothing | $150 |

Personal Care | $80 |

Vacation Fund | $200 |

House Down Payment | $800 |

Emergency Savings | $250 |

Total | $4,000 |

Mia’s savings envelopes (“House Down Payment,” “Emergency Savings,” “Vacation Fund”) are just as important as her spending envelopes. The digital app automatically tracks her balances, and she checks them before making any purchase over $50.

Example 3: Family of Four

The Martins have two children and a combined take‑home pay of $6,200. They use a hybrid system: cash for variable day‑to‑day spending, bank autopay for fixed bills, and automatic transfers for long‑term savings.

Envelope | Monthly Amount |

|---|---|

Mortgage | $1,600 |

Utilities | $350 |

Groceries (cash) | $900 |

Car Payment | $300 |

Gas (cash) | $200 |

Childcare | $800 |

Kids’ Activities (cash) | $150 |

Dining Out (cash) | $100 |

Family Entertainment (cash) | $100 |

Clothing (cash) | $150 |

Medical/Dental | $200 |

Emergency Fund | $300 |

Vacation Fund | $150 |

Total | $6,200 |

The Martins hold a weekly family meeting to review the envelopes. The kids see the cash and understand that when the “Dining Out” envelope is empty, they eat at home. This visual system has reduced arguments about money and taught the children basic budgeting.

Example 4: Freelancer with Irregular Income

Dev is a freelance writer whose income swings between $2,500 and $5,000 a month. He uses a baseline budget based on his lowest income month and treats any surplus as a bonus to be allocated later.

Envelope (Baseline: $2,500) | Monthly Amount |

|---|---|

Rent | $950 |

Utilities | $180 |

Groceries | $350 |

Transport | $100 |

Insurance | $150 |

Phone/Internet | $90 |

Personal Care | $60 |

Emergency Savings | $200 |

Tax Reserve | $200 |

Miscellaneous Buffer | $220 |

Total | $2,500 |

When Dev earns more than $2,500, he applies a priority list: first, he tops up his tax reserve (he sets aside 25% of any surplus for taxes); second, he adds to his emergency fund until it reaches three months of expenses; third, he puts money into a “Business Growth” envelope for equipment and courses; and finally, he treats himself. In lean months, he relies on the buffer and reduces discretionary spending.

Common Envelope Budgeting Mistakes

Even a simple system can be undermined by a few common errors.

Mistake | Why It Happens | How to Avoid It |

|---|---|---|

Forgetting irregular expenses | Annual bills aren't top of mind | Create a "Sinking Funds" envelope for insurance, car registration, etc. |

Using envelopes inconsistently | Caving to convenience | Start with a month‑long commitment; pair with a visual reminder |

Borrowing from other envelopes | Rationalizing that you'll "pay it back" | Treat each envelope as a firm boundary; adjust the budget only at month‑end |

Unrealistic amounts | Estimating based on ideals, not history | Base categories on past spending; track for two weeks before setting limits |

Ignoring savings | Treating savings as optional | Create a dedicated savings envelope and fund it first |

Not reviewing monthly | Forgetting to evaluate and tweak | Schedule a 30‑minute review at the end of each month |

Carrying too much cash | Over‑withdrawing for convenience | Only withdraw what you need for a week or two at a time |

Failing to track cash spending | Forgetting to record purchases | Keep a small notebook or use a notes app; reconcile daily |

The biggest mistake is giving up after one rough month. Envelope budgeting is a skill. The first month often reveals that your initial estimates were off; that’s feedback, not failure.

Tips for Success

Start with three to five categories. You don’t need a dozen envelopes on day one. Pick the areas where you overspend most—groceries, dining out, shopping—and expand as you get comfortable.

Track every expense for the first two weeks. Before setting final envelope amounts, carry a small notebook and jot down every purchase. This reveals patterns you’d otherwise miss.

Review and adjust monthly. Life changes. Your budget should too. If you consistently blow the grocery envelope by $50, either find ways to trim or increase the envelope and reduce another.

Keep your savings envelope physically separate. Don’t store your emergency fund with your spending envelopes. Use a separate bank account or a sealed envelope stored safely. This reduces temptation.

Use digital tools if cash isn’t practical. Plenty of free apps replicate the envelope method digitally. You can also set up sub‑accounts at some banks or use a simple spreadsheet with running balances.

Build an emergency fund first. Before aggressively paying down debt or saving for a vacation, ensure you have at least a small cash cushion. This prevents a single unexpected bill from upending your entire budget.

Stay consistent for 90 days. It takes roughly three months for a new financial habit to feel automatic. Commit to the system for that period before deciding whether to keep it or switch.

Frequently Asked Questions

What is the Envelope Budgeting Method?

The Envelope Budgeting Method is a spending system where you allocate cash into envelopes representing different expense categories. You spend only from the designated envelope, and when it’s empty, spending in that category stops. This approach creates a tangible limit that can help reduce overspending.

Does envelope budgeting really work?

Yes, for many people it does. The method works by introducing psychological friction to spending. Handling cash makes the cost feel real, which studies show can reduce impulse purchases. Success depends on setting realistic envelope amounts and sticking to the rule of stopping when an envelope is empty.

Is envelope budgeting only for cash?

No. While the traditional method uses physical cash, digital versions exist. You can replicate the system with budgeting apps, bank sub‑accounts, or a spreadsheet that tracks allocated amounts per category. The core principle—limiting spending by category—works digitally as long as you monitor balances consistently.

Can I use envelope budgeting digitally?

Absolutely. Many budgeting apps offer envelope‑style features where you assign money to virtual envelopes. Alternatively, you can manually track envelope balances in a spreadsheet. The key is to check the balance before making a purchase, just as you would count the cash in a physical envelope.

What happens if an envelope is empty?

You stop spending in that category until the next budgeting period—usually the following month. If the expense is urgent, you can reallocate money from another envelope, but this should be a deliberate decision made before the purchase, not an automatic habit. Regular shortfalls signal that the envelope amount needs adjusting.

How many envelopes should I have?

There’s no magic number. Start with categories where you tend to overspend, such as groceries, dining out, and entertainment. Most people end up with 5 to 10 spending envelopes, plus separate ones for savings and irregular expenses. Too many envelopes can become unmanageable.

Can couples use envelope budgeting?

Yes, and it can improve financial communication. Couples can maintain separate envelopes for personal discretionary spending and shared envelopes for household expenses. They need to agree on the amounts and communicate when an envelope is running low.

Is envelope budgeting good for debt repayment?

Yes. By capping spending, the envelope method often frees up money that can be directed to debt. You can create a specific “Debt Repayment” envelope and treat it as a priority. The system also prevents new credit card debt because you’re spending pre‑allocated cash.

How does it compare with the 50/30/20 rule?

The 50/30/20 rule provides a broad framework—50% needs, 30% wants, 20% savings—but doesn’t limit specific categories. Envelope budgeting offers more granular control. Many people blend the two: using 50/30/20 as a guideline to set overall envelope amounts.

Is envelope budgeting suitable for irregular income?

Yes, with adjustments. Build a baseline budget based on your lowest recent monthly income. When you earn more, allocate the surplus according to a priority list—first to essentials, then savings, then discretionary envelopes. This smooths out income fluctuations.

Can I use credit cards with envelope budgeting?

It’s possible if you track each credit card purchase against the envelope balance and pay the card in full each month. However, this removes the tactile cash‑limiting effect. It requires strong discipline, so most people find cash or debit cards more effective for envelope budgeting.

Should savings have its own envelope?

Yes. Treating savings as a non‑negotiable expense helps you build an emergency fund, save for large goals, and pay yourself consistently. Keep the savings envelope physically separate—ideally in a bank account—so it’s not easily tapped for daily spending.

How often should I review my budget?

At minimum, do a brief weekly check to see which envelopes are getting low, and a full review at the end of each month. The monthly review is where you adjust amounts based on actual spending and evaluate whether the envelope allocations still match your priorities.

What expenses should not use envelopes?

Fixed automatic bills—rent, mortgage, utilities, insurance—can be left in your bank account. Envelopes work best for variable, discretionary categories where overspending is common. Trying to use cash for everything is unnecessarily cumbersome.

Is envelope budgeting outdated?

Not at all. While it originated in an era of cash transactions, the underlying principle—creating hard limits on spending—remains effective. Digital versions have modernized the method for an online‑shopping world without losing its core behavioural benefit.

Does envelope budgeting help stop overspending?

For many people, yes. The physical or visual limit of an emptying envelope creates a natural stop signal. It interrupts the mindless spending that can happen with credit cards, replacing it with conscious decision‑making. Studies on the “pain of paying” support its effectiveness.

Can beginners use envelope budgeting?

It’s one of the most beginner‑friendly methods because it’s intuitive. There are no complex formulas—just envelopes, cash, and simple rules. Beginners should start with a few categories and expand as they gain confidence.

How do I handle unexpected expenses?

Build a “Miscellaneous” or “Buffer” envelope for small surprises. For larger unexpected costs, draw from your emergency fund—which should be a separate, well‑funded envelope or account. After the expense, prioritize replenishing the emergency fund.

What’s the biggest mistake people make?

Giving up too quickly. The first month is often frustrating because initial envelope amounts rarely match reality. It takes two to three months of tweaking to dial in the numbers. Treat early missteps as data, not failure, and adjust.

Is envelope budgeting right for everyone?

No single method works universally. If you value extreme simplicity and hate handling cash, envelope budgeting may feel burdensome. But if you’re a visual learner who struggles with impulse spending, it’s one of the most effective tools available.

Table 1 — Envelope Budgeting Overview

Feature | Description |

|---|---|

Core Principle | Allocate cash (or digital equivalents) to labeled envelopes; stop spending when empty |

Primary Goal | Prevent overspending by making limits tangible |

Typical Envelope Count | 5–10 spending categories plus savings and irregular expenses |

Time Commitment | Moderate; requires setup, withdrawals, and monthly reviews |

Best For | Overspenders, beginners, families, visual/tangible learners |

Table 2 — Physical vs Digital Envelopes

Aspect | Physical Cash Envelopes | Digital Envelope Systems |

|---|---|---|

Spending Awareness | Very high | Moderate (depends on app usage) |

Security | Cash can be lost or stolen | Digital protection, but accounts can be hacked |

Convenience | Inconvenient for online purchases | Convenient for all payment types |

Best Users | Overspenders, visual learners, those who prefer cash | Tech‑savvy users, online shoppers, card‑dependent spenders |

Setup | Simple (envelopes + cash) | Requires app setup and linking accounts |

Cost | Free (envelopes) | Some apps charge subscription fees |

Table 3 — Monthly Envelope Categories (Typical)

Category Type | Examples |

|---|---|

Fixed Essentials | Rent/Mortgage, Utilities, Insurance, Minimum Debt Payments |

Variable Essentials | Groceries, Gas/Transport, Medical |

Discretionary | Dining Out, Entertainment, Shopping, Personal Care |

Savings Goals | Emergency Fund, Vacation, Down Payment, Education |

Irregular/Sinking Funds | Car Repairs, Annual Subscriptions, Holiday Gifts |

Table 4 — Example Monthly Budget Allocation

Envelope Category | Single Professional ($4,000/mo) | Family of Four ($6,200/mo) |

|---|---|---|

Housing | $1,400 | $1,600 |

Utilities | $200 | $350 |

Groceries | $450 | $900 |

Transport | $120 | $500 (car + gas) |

Dining Out | $200 | $100 |

Entertainment | $150 | $100 |

Shopping/Clothing | $150 | $150 |

Personal Care | $80 | — |

Childcare | — | $800 |

Kids’ Activities | — | $150 |

Medical/Dental | — | $200 |

Vacation Fund | $200 | $150 |

Emergency Savings | $250 | $300 |

House Down Payment / Other | $800 | — |

Total | $4,000 | $6,200 |

Table 5 — Advantages and Disadvantages

Advantages | Disadvantages |

|---|---|

Tangible spending limits reduce impulse buys | Inconvenient for online shopping and automatic bills |

Simple to understand and implement | Cash handling can feel unsafe or tedious |

No need for complex software | Less effective if you share envelopes without communication |

Builds discipline through clear rules | Requires regular trips to the bank/ATM |

Frees up money for debt and savings | Initial envelope amounts often need several months of adjustment |

Reduces reliance on credit cards | Can feel overly restrictive and lead to abandonment |

Table 6 — Envelope Budgeting vs Other Methods

Method | Control Level | Flexibility | Automation | Best For |

|---|---|---|---|---|

Envelope Budgeting | Very High | Low | Low | Overspenders, hands‑on budgeters |

Zero‑Based Budgeting | High | Medium | Medium | Detail‑oriented planners |

50/30/20 Budget | Low to Moderate | High | High | Beginners, simplicity seekers |

Pay‑Yourself‑First | Low (saving) / Low (spending) | High | High | Busy professionals |

Traditional Budget | Low | Medium | Low | People who want a light framework |

Table 7 — Common Mistakes and Solutions

Mistake | Solution |

|---|---|

Forgetting irregular expenses | Create sinking fund envelopes for annual bills |

Using envelopes inconsistently | Commit to a 30‑day trial; set a daily reminder to check envelopes |

Borrowing between envelopes | Reallocate only during the monthly review, not mid‑month |

Unrealistic amounts | Base amounts on tracked spending history |

Neglecting savings envelopes | Fund savings envelopes first |

Not reviewing monthly | Schedule a recurring 30‑minute review session |

Quitting after a rough month | Expect a learning curve; use early months as data gathering |

Table 8 — Best Users for Envelope Budgeting

User Profile | Why It Works |

|---|---|

Overspenders | Tangible limits create friction that cards lack |

Beginners | Simple, no formulas, intuitive |

Families | Visual system that can involve the whole household |

Students | Limited income needs strict management |

Debt Repayers | Caps spending to maximize debt payments |

Low‑to‑Moderate Income | Every dollar’s job is visible and protected |

Table 9 — Real‑Life Budget Scenarios at a Glance

Scenario | Income | Method Used | Key Envelope Categories |

|---|---|---|---|

College Student | $1,200/mo | Cash envelopes + autopay | Groceries, Dining Out, Entertainment, Savings |

Single Professional | $4,000/mo | Digital envelope app | Rent, Groceries, Dining Out, Down Payment Fund |

Family of Four | $6,200/mo | Hybrid cash + autopay | Mortgage, Groceries, Childcare, Emergency Fund |

Freelancer | Variable ~$2,500–$5,000 | Baseline budget with surplus allocation | Tax Reserve, Emergency Fund, Buffer, Business Growth |

Table 10 — Envelope Budgeting Success Checklist

Action Item | Frequency |

|---|---|

Calculate net monthly income | Monthly |

Set envelope categories and amounts | Monthly |

Withdraw cash / fund digital envelopes | Start of month |

Track spending against envelopes | Weekly or after each purchase |

Adjust envelopes if necessary | Only at month‑end |

Review overall budget and goals | Monthly |

Replenish emergency fund if depleted | As soon as possible |

Evaluate whether the method is working | Quarterly |

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, tax, or professional advice. Budgeting methods and financial strategies should be adapted to individual circumstances, including income, expenses, financial goals, household size, and lifestyle. Readers should evaluate their own financial situation or consult a qualified financial professional before making significant financial decisions.

Recommended Articles

The Complete Guide to Budgeting for Beginners

Budgeting isn’t about restriction—it’s about clarity. A realistic, no-shame guide for beginners to understand where your money goes, build a system that sticks, and finally end the guilt cycle.

50/30/20 Budget Rule Explained (With Real-Life Examples)

Struggled with budgets that never stick? Learn the 50/30/20 rule with real-life examples, honest limitations, and practical steps to finally take control of your money.